SHIP market declines in 2025 despite broad industrial adoption

April 29, 2026

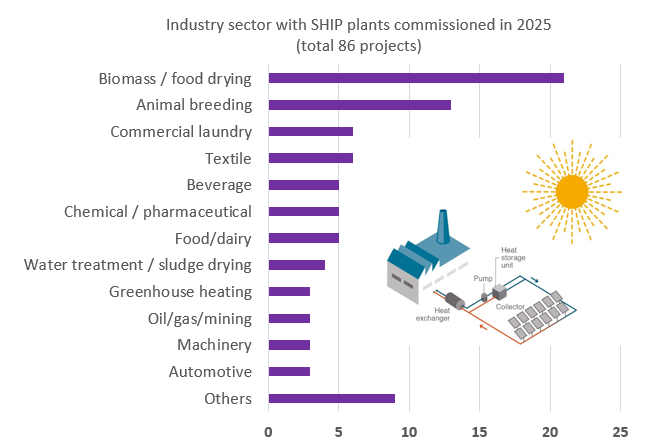

In 2025, solar heat for industrial processes (SHIP) continued to be deployed across a broad range of industrial sectors, as illustrated in the chart above. Drying processes and barn heating systems accounted for the majority of new installations, while steam applications in the chemical and pharmaceutical industries were also among the systems commissioned last year across 18 countries worldwide. However, the global SHIP market contracted significantly compared to previous years. In 2025, project developers reported a total of 86 new systems with a combined capacity of 28 MW, down from 106 systems and 120 MW in 2024. This downturn is expected to be temporary, as two large collector fields with a combined capacity of 113 MW are currently under construction for the copper mine Minera Escondida in Chile and are at an advanced stage, with commissioning anticipated end of this year or early next year. You can also read the news about the Solar Industrial Heat Outlook 2026-2028 here. Graphic: solrico

The weaker market performance in 2025 can be attributed to several factors, including the continued decline of the Dutch SHIP market following changes to the subsidy scheme in 2024, as well as delays in a number of large-scale projects that had been announced earlier. In response to these challenging conditions, project developers are increasingly offering hybrid solutions (see related news article). The survey was conducted by the German agency solrico in the first quarter of 2026, with support from Natural Resources Canada.

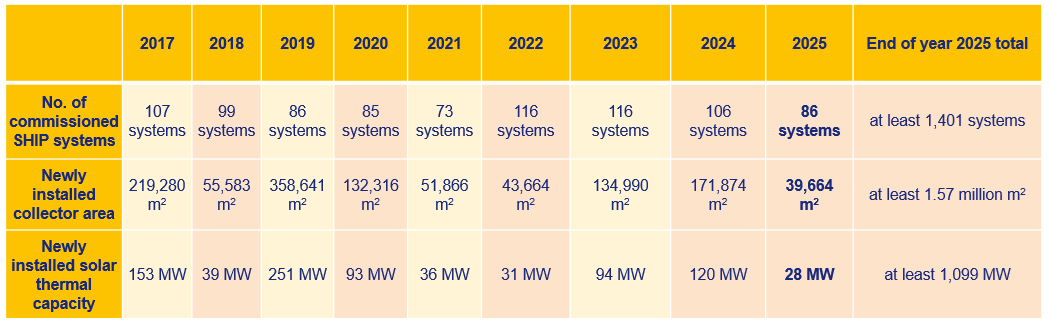

Table 1 illustrates the development of the SHIP market over recent years, highlighting significant fluctuations. The 86 new systems installed in 2025 bring the market back to the lower levels observed in 2020 (85 systems) and 2021 (74 systems).

Table 1: Global SHIP market development between 2017 and 2025. The large fluctuations in added capacity are the result of large capacity additions in Oman and China in certain years. Capacity was calculated using the factor 0.7 kW/m2 for all collector types. Source: Annual surveys carried out by solrico between 2017 and 2026 of the companies listed on the Turnkey SHIP Supplier World Map: https://www.solar-payback.com/suppliers/

“Customer decisions are being delayed”

When asked about the challenges involved in SHIP project development, the participating companies pointed to the long decision-making processes among industrial clients – from the initial feasibility studies through to implementation and the start of construction.

An internationally active project developer from the Benelux countries summarized the situation as follows: “Customer decisions are being delayed due to general economic conditions, lower gas prices and reduced pressure to decarbonize.”

A project developer from Austria added: “The market is highly competitive, but clients are still reluctant to adopt solar thermal solutions due to low energy prices (gas, electricity). The market is strongly driven by policy and subsidies, which are more focused on heat pumps. Solar process heat still requires significant effort in sales development.”

Project developers are responding to the challenging market environment, with some of them offering hybrid solutions – that is, solar collector fields combined with heat pumps or storage systems – to significantly increase the proportion of renewable energy used for heating throughout the year. You can read more about this trend in a separate article to be published on solarthermalworld.org soon.

An upturn in the global solar market is expected again in 2026, as several large-scale projects are currently under construction, including this 7.3 MW parabolic trough field (shown here in a photomontage) for the Heineken brewery in Greece. In addition, the two flat-plate collector fields for the Minera Escondida copper mine in Chile (90 and 23 MW) have already been completed, and the main supply lines to the copper processing plant are currently being laid, as confirmed by consultant Ian Nelson. Photo: Protarget

SHIP market development on a national level

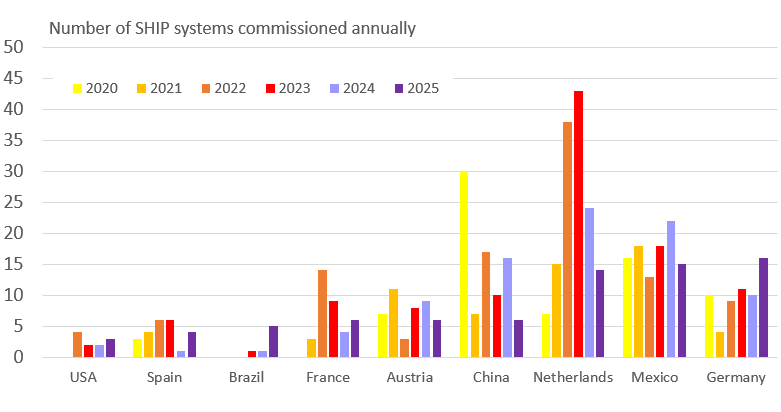

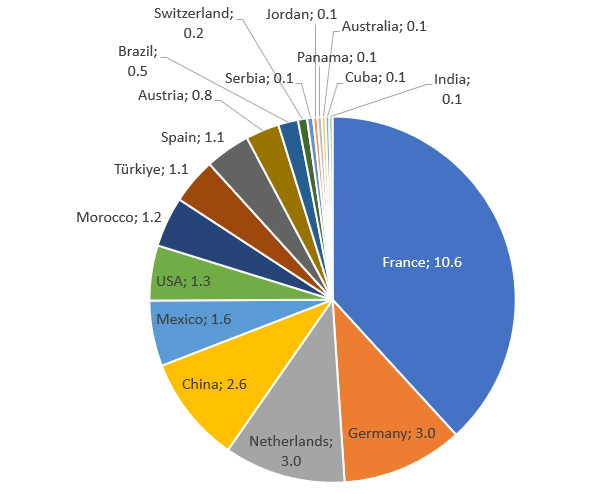

The statements indicate that the solar heat for industrial processes (SHIP) market – particularly in Europe – still depends heavily on investment subsidies to remain competitive with low gas and oil prices and to offset high upfront costs. As a result, changing policy frameworks are causing significant fluctuations in leading SHIP markets in terms of new installations, as illustrated in figure 1. For a clearer understanding of national market developments, figure 1 should be considered alongside figure 2, which presents newly installed SHIP capacity by country in 2025.

Germany ranks first in figure 1 with 16 new installations. This is largely due to the long-term subsidy scheme “EEW Module 2: Process Heat from Renewables”, which covers between 40 % and 60 % of SHIP system investment costs, depending on the size of the investor. However, system sizes remain relatively small despite the absence of an upper funding limit. In total, only 3 MW of new SHIP capacity was installed in Germany (figure 2), corresponding to an average system size of 265 m².

France represents the second European country with a long-term subsidy scheme supporting large-scale solar heat systems including industrial applications, administered by the French agency ADEME. In contrast to Germany, multi-megawatt-scale systems are actively applied for and implemented in France. As a result, France takes the top position in figure 2, with 10.6 MW of newly installed SHIP capacity. This includes two greenhouse heating projects: one developed, designed and built by New Heat (5 MW for tomato production in southern France) and another by the Finish collector manufacturer and project developer Summa Energy Oy formerly Savosolar (4 MW for a vegetable producer near the Spanish border). With a total of six new installations, France ranks sixth in figure 1. A comparison between Germany and France – both offering strong, long-term subsidy schemes – suggests that Germany currently lacks project developers willing to undertake large-scale SHIP projects. However, this may change as one larger grant was awarded for a 38 MW parabolic trough system for a metal-processing company in northern Germany, with funding amounting to EUR 19 million. Implementation of the plant, however, has not yet started.

Mexico ranks second in terms of the number of newly installed SHIP systems in 2025, with 15 projects. However, this represents a decline compared to previous years (22 projects in 2023 and 18 in 2024). According to one project developer: “There are no government policies promoting the use of SHIP technologies. A project planned for 2025 was postponed due to a lack of client investment capital.” In 2025, most installations were in the textile industry and large-scale laundries, totalling 1.6 MW.

The Dutch market has been negatively affected by a 30 % reduction in subsidy levels under the ISDE scheme at the beginning of 2024. As a result, the number of newly installed SHIP systems declined sharply from 43 in the peak year 2023 to just 14 in 2025. This drop is one of the factors contributing to the weak global SHIP market in 2025. Newly installed capacity amounts to 3 MW, consisting of relatively small systems averaging 303 m², primarily in the agricultural sector.

China, ranking fourth in figure 1 with six systems (2.6 MW in total), remains a complex and fragmented market. The reported data may only reflect part of the overall market activity. In general, major collector manufacturers in China focus primarily on project development for residential housing areas or hotels, while SHIP systems for industrial clients are only rarely planned and implemented.

In Austria, six systems were installed in 2025; however, these were exclusively small-scale agricultural drying systems, using either air collectors or flat-plate collectors. Funding for large-scale solar thermal systems from the Climate and Energy Fund ended in December 2023. According to the program administrator, around 20 projects from the funding scheme are still awaiting completion. “The budget of the Climate and Energy Fund has been significantly reduced and no further calls for proposals are currently planned”, reports Gernot Wörther from the fund. As a result, the SHIP market in Austria is unlikely to receive further momentum from public funding in the near future.

Brazil appears for the first time among the top countries in terms of new SHIP installations. In 2025, five systems with a total capacity of 0.5 MW were installed in the beverage industry. Four of these projects were implemented through a public call under the National Energy Conservation Programme for Industry (PROCEL) and financed with government funds dedicated to energy efficiency and renewable energy initiatives. Further market growth in Brazil can be expected in the coming years.

Figure 1: Top markets in terms of the number of new SHIP plants commissioned per year between 2020 and 2025. Brazil was added to the ranking for the first time this year with 5 new systems commissioned in 2025. Source: Annual surveys of the companies listed on the SHIP Supplier World Map

Figure 2: SHIP capacity additions in 2025 in MW per country. In total, SHIP installations with 28 MW started operation worldwide last year. Capacity was calculated using the factor 0.7 kW/m2 for all collector types. Source: Survey 2026 of companies listed on the SHIP Supplier World Map

Delays in large-scale projects weigh on SHIP market growth

The SHIP market in 2025 was characterized by small-scale systems. The average collector area of the 86 newly installed plants was 461 m². This was partly due to significant delays in the implementation of several large-scale projects.

- One example is the plant for Boortmalt in Croatia, featuring a 20 MW collector field, for which New Heat received a EUR 4.5 million grant from the Innovation Fund as early as 2021. The project is still in the planning phase, and construction has not yet started.

- Delays have also affected the implementation of an 18 MW parabolic trough collector field for Mars Petcare in Victoria, Australia. Although the project was officially launched in autumn 2024, complications arose when the Belgian EPC contractor Azteq, which had been awarded the contract for the collector field, filed for insolvency in December 2024. Despite its challenges, Mars has reaffirmed its commitment to the project. The Australian Renewable Energy Agency (ARENA) had granted AUD 17 million for the solar field.

- In Latin America, a 12 MW project was put on hold by the client, even though civil works had already begun and the collector field site was largely prepared. The main reason cited was heightened uncertainty in the region linked to US government policies.

- Another example comes from France, where ADEME approved funding for an installation of about 12 MW in the beverage industry in 2023. The project remains in the preparation phase, and construction has yet to begin.

Such prolonged project development timelines pose a serious risk to the expansion of solar thermal technologies, which represent an important pillar for reducing CO₂ emissions in industry.

Websites of organizations mentioned in this news article:

Solrico: https://www.linkedin.com/in/b%C3%A4rbel-epp-510b74b2/

Natural Resources Canada: https://natural-resources.canada.ca/

Turnkey SHIP Supplier World Map: https://www.solar-payback.com/suppliers/

ADEME: https://www.ademe.fr/en/frontpage/

New Heat: https://newheat.com/en/

Summa Energy Oy (formerly Savosolar): https://summaenergy.com/en/home/

Climate and Energy Fund: https://www.klimafonds.gv.at/

PROCEL: https://www.procel.gov.br/sites/dev/SitePages/Home.aspx

Boortmalt: https://www.boortmalt.com/

Mars Petcare: https://www.mars.com/en-au/our-brands/petcare

ARENA: https://arena.gov.au/