IEA SHC: 20 Country Profile Analyse Market and Industry Development

September 3, 2015

“The Renewable Heat Incentive in the United Kingdom has failed to stimulate the market for solar thermal, which continues to contract. There are technical issues in the regulations preventing the use of solar thermal with other renewable heating systems, such as biomass and heat pumps, and the subsidy rate is relatively low compared to the feed-in tariff for solar photovoltaics.” This clear statement was made by Dr Robert Edwards, Director in the Science and Innovation Group at the Department of Energy and Climate Change (DECC). He represents the country in the Executive Committee of the IEA Solar Heating and Cooling (SHC) research programme and delivered an updated country profile of the British solar thermal market in June 2015. As part of its services, the IEA SHC programme publishes updated market profiles of all 20 member countries each year. You will find the list of member countries online and the link to the country profile at the bottom of each country page. The statement by Edwards is part of the latest UK country profile.

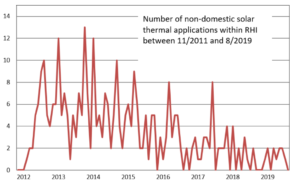

The country profile deliver a comprehensive view on the market, including latest sales volumes, an analysis of major market drivers and barriers, a view into the national supply chain, some figures on system costs and political frame conditions, as well as a chapter on current innovations in the solar heating and cooling industry. The following text includes some of the figures from the UK country profile and the latest statistics on the Domestic RHI delivered by the Gas and Electricity Markets Authority, Ofgem.

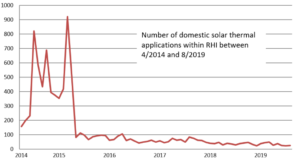

Although the long-awaited Domestic Renewable Heat Incentive (Domestic RHI) came into force in April 2014, sales volume decreased again last year for the fourth time in a row, down to 36,552 m² (-15 %). Edwards listed three major barriers:

- Cheaper and rapidly falling PV prices compared to solar thermal

- Lack of demonstration projects by large building developers

- Lack of sector coordination to remove market barriers

The application figures of the Domestic RHI confirm the analysis by Edwards when he mentioned the imbalance between the different renewable heating technologies. Solar thermal is still lagging behind a great deal in this year`s statistic (see the following table). The growth in demand for newly installed solar water heaters is much lower than for biomass boilers or heat pumps.

|

Applications for |

Applications for |

Increase |

|

| Solar thermal |

344 |

1,278 |

272 % |

| Air-source heat pumps |

540 |

2,939 |

444 % |

| Ground-source heat pumps |

93 |

591 |

535 % |

| Biomass boilers |

778 |

5,143 |

561 % |

| Total |

1,755 |

9,951 |

467 % |

Comparison of Domestic RHI applications last year and this year. The figures for 2014 were taken from earlier statistical news, the figures for 2015 from the quarterly report (see the attached quarter report)

Source: Ofgem

The spending balance also shows an unequal distribution between technologies. According to the first year’s balance covering 9 April 2014 to 31 March 2015 (see the attached first annual report), Pound Sterling (GBP) 16.3 million were spent in total on renewable heat technologies, of which 55 % were spent on biomass, 41 % on both heat pump types and only 3 % on solar thermal. The administrators of the Domestic RHI responded to the unexpectedly high uptake of biomass boilers by using a so-called degression trigger. In April 2015, the tariff for biomass heat was reduced by 20 % to 0.0714 GBP/kWh, and it was planned to be reduced again by 10 % in October 2015, as announced in a press release from DECC on 28 August 2015.

Other interesting aspects from the UK country profile by the IEA SHC:

- The domestic collector manufacturers – Viridian Solar, Thermatwin and AES Solar – together account for approximately 10 to 15 % of annual market volume.

- Among the current innovative drivers is the company Naked Energy, which has developed a PVT collector in which the PV cells are linked to a patented heat plate absorber, with both being placed into an evacuated tube.

- So-called Transpired Solar Collectors (TSCs), which are unglazed air collectors used on the façade, are growing in market share in the UK. According to the country profile, there are currently 14,000 m² of TSCs installed at 33 industrial and commercial buildings in the UK. A number of the UK´s largest industrial cladding companies now have TSCs as part of their standard product offering.

More information:

Statistics of the Domestic RHI: https://www.ofgem.gov.uk/

Country members of the IEA SHC: http://www.iea-shc.org/members

Department of Energy and Climate Change: http://www.gov.uk/government/organisations/department-of-energy-climate-change