UK: How Does Solar Thermal Sustain against Photovoltaics and Biomass?

November 30, 2017

At the end of 2016 the solar thermal industry association STA campaigned successfully for solar thermal to remain in the two Renewable Heat Incentives (RHI). However, the year 2017 was so far weaker than the previous years. In the domestic RHI there were 423 residential applications accredited from January to September 2017, compared to 537 in the same period of the previous year. Approved applications for commercial solar thermal plants with in the non-domestic RHI were down to 19 in this same period from 36 in the previous year. The photo shows a 155 m² installation on the roof of the new Star Community Centre in Cardiff that opened its doors in September 2016.

At the end of 2016 the solar thermal industry association STA campaigned successfully for solar thermal to remain in the two Renewable Heat Incentives (RHI). However, the year 2017 was so far weaker than the previous years. In the domestic RHI there were 423 residential applications accredited from January to September 2017, compared to 537 in the same period of the previous year. Approved applications for commercial solar thermal plants with in the non-domestic RHI were down to 19 in this same period from 36 in the previous year. The photo shows a 155 m² installation on the roof of the new Star Community Centre in Cardiff that opened its doors in September 2016. Photo: Kingspan

The reasons for this poor market performance are twofold: The photovoltaics market is much stronger compared with the solar thermal domestic RHI (dRHI) with customers perceiving better tariff conditions. On average 2,980 residential PV installations were accredited over the last two quarters against only 55 residential solar thermal accreditations monthly.

In 2017 domestic solar thermal systems receive 0.2006 Pound Sterling (GBP) per kWh (0.26708 USD/kWh) over 7 years with only minor adjustments for inflation over the year. The energy (kWh) for the dRHI is deemed by a calculation by the installer whereas the RHI (non-domestic) is measured by a meter (see further details in the database of incentive programmes: RHI and dRHI). To compare the tariffs with the PV feed-In incentive for sub 10 kW, this currently receives 0.040 GBP/kWhel (0.0533 USD/kWhel) over 20 years plus 0.0503 GBP/kWh (0.067 USD/kWhel) fed to the grid.

The second reason is the stronger demand for other renewable heat technologies like air source heat pumps and biomass boilers that take together 80 % of all approved applications (see table 1). Of all the dRHI technologies only solar thermal is not allowed to contribute to space heating.

|

Air source heat pump |

Ground source heat pump |

Biomass systems |

Solar Thermal |

Cumulative totals |

|

| Cumulative totals |

16,121 |

3,522 |

9,206 |

3,228 |

32,077 |

| % |

50.3% |

11.0% |

28.7% |

10.1% |

|

Accredited applications for the domestic RHI since the start of the programme in April 2014 through to September 2017. For Northern Ireland since March 2016 the (RHI) has been suspended to new applications for all technologies. No figures for Northern Ireland are included in these statistics.

Source: Ofgem

Solar thermal often combined with gas boiler

The UK government provided additional dRHI statistics which provide further useful characteristics of the national solar thermal market in single-family households. For example with all other dRHI technologies the majority of installations favoured away from the main natural gas network. But for solar thermal in England the majority were fitted in properties on the gas grid. When considering the type of house that ST was fitted, the owner or occupier detached house was the most likely type even compared to all other house types added together. These included semi-detached, terraced, bungalow, flat or maisonette. Although 78% of household ST was fitted in England, the three most likely regions were Southeast England, Southwest England and Scotland.

Overall 17,000 non-domestic renewable installations under RHI

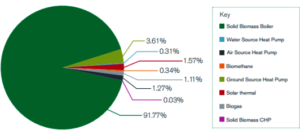

All in all the non-domestic RHI was so far rather successful with 17,636 renewable heating systems under contract by the end of September 2017. However, only 1.6 % – 274 solar thermal systems in total – are among them (see table below). Biomass usage is absolutely dominating this scheme. The non-residential RHI allows solar thermal fields below 200 kW and pays 0.1044 Pound Sterling (GBP) per kWh over 20 years (see further details in the database of incentive programmes: RHI and dRHI). For comparison biomass has various power thresholds from between 0.0208 to 0.0296 GBP/kWh over 20 years with no top limit.

|

Heat Pumps |

Biomass |

CHP |

Biogas / Biomethane |

Solar Thermal |

Cumulative totals |

|

| Cumulative totals |

1,179 |

15,621 |

29 |

533 |

274 |

17,636 |

| % |

7.0% |

88.6% |

0.2% |

3.0% |

1.6% |

|

Accredited applications for the non-residential RHI since the start of the programme in November 2011 through to September 2017. No figures for Northern Ireland are included in these statistics.

Source: Ofgem

Source: Ofgem

Websites of institutions and companies mentioned in the text:

OFGEM: http://www.ofgem.gov.uk/environmental-programmes

Department for Business, Energy & Industrial Strategy: http://www.gov.uk/beis